Planning to take a home loan, personal loan or a credit card. You definitely want to make sure it is approved and processed quickly? I am sure you will look for a loan at a lower interest rate? In addition to other financial tools like credit cards, many banks, NBFCs, and other financial organizations also provide loans to individuals. From your income, occupation, work experience, to your age, there are a lot of things that loan and credit card providers in India take into consideration before approving your application. While these factors are very important too, your Credit score is probably the most important. Even if you do meet all the other eligibility requirements of a bank, it is very much possible for your loan or credit card application to be rejected if you have a poor credit score. So what is credit score and why it is so important for every borrower ?

What is CIBIL Score?

There are four companies licensed by the RBI (Reserve Bank of India) to function as credit information companies. They are Experian, Equifax ,CIBIL and Highmark. However, the most popular credit score in India is the CIBIL score.The Credit Information Bureau (India) Limited (CIBIL) is the most popular of the four.CIBIL Limited maintains credit files on 600 million individuals and 32 million businesses.

CIBIL India is part of TransUnion, an American multinational group. Hence credit scores are known in India as the CIBIL Transunion score.The banks and credit card providers in India are its members. These members share the account information of its loan and credit card customers with CIBIL.

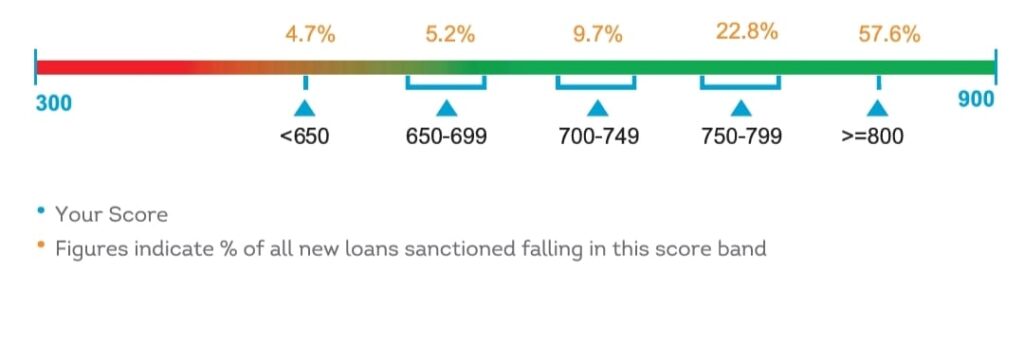

CIBIL Score is a three-digit number ranging between 300 and 900, which TransUnion CIBIL publishes. It collates and stores credit-related information from banks and NBFCs about individuals and corporate houses. Then, based on the available data and the credit history, it prepares a report and issues credit scores.1

- The Score Varies from 300-900. ↩︎

What is CIBIL Report

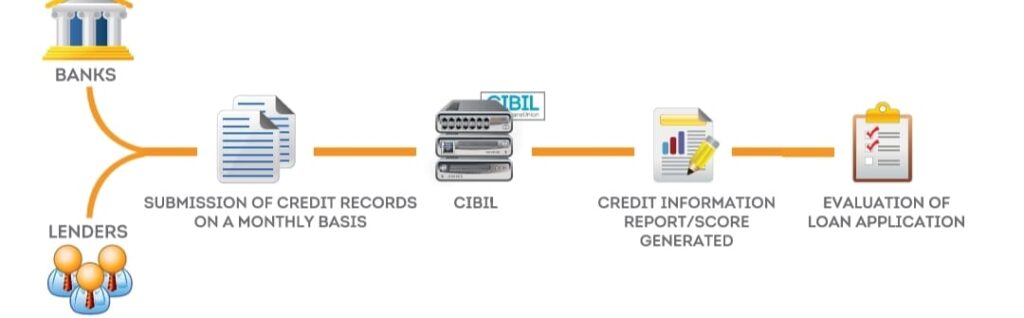

Transunion CIBIL Limited is India’s first credit information company . They collect and maintain monthly reports( credit information reports -CIR) from banks and financial institutions, detailing individual loan and credit card payment history. Basis the CIR a credit score is generated which is then used by the lenders during the loan evaluation process.

Source: CIBIL.com

Credit score is derived by using details found in the accounts and enquiries section on your credit information report.It indicates the probability of default of a borrower based on their credit history.

Benefits of High CIBIL Score

- Lower rate of interest

- Loan with longer Term

- Faster Loan/Credit card approval

- Avoid several loan inquiries/applications at the same time.

- Approval for higher limits.

- Improved negotiating position

- Outstanding credit card offers

- Pre-approved loans are available

- A reduction in loan processing fees and other costs

What happens if you have bad CIBIL Score

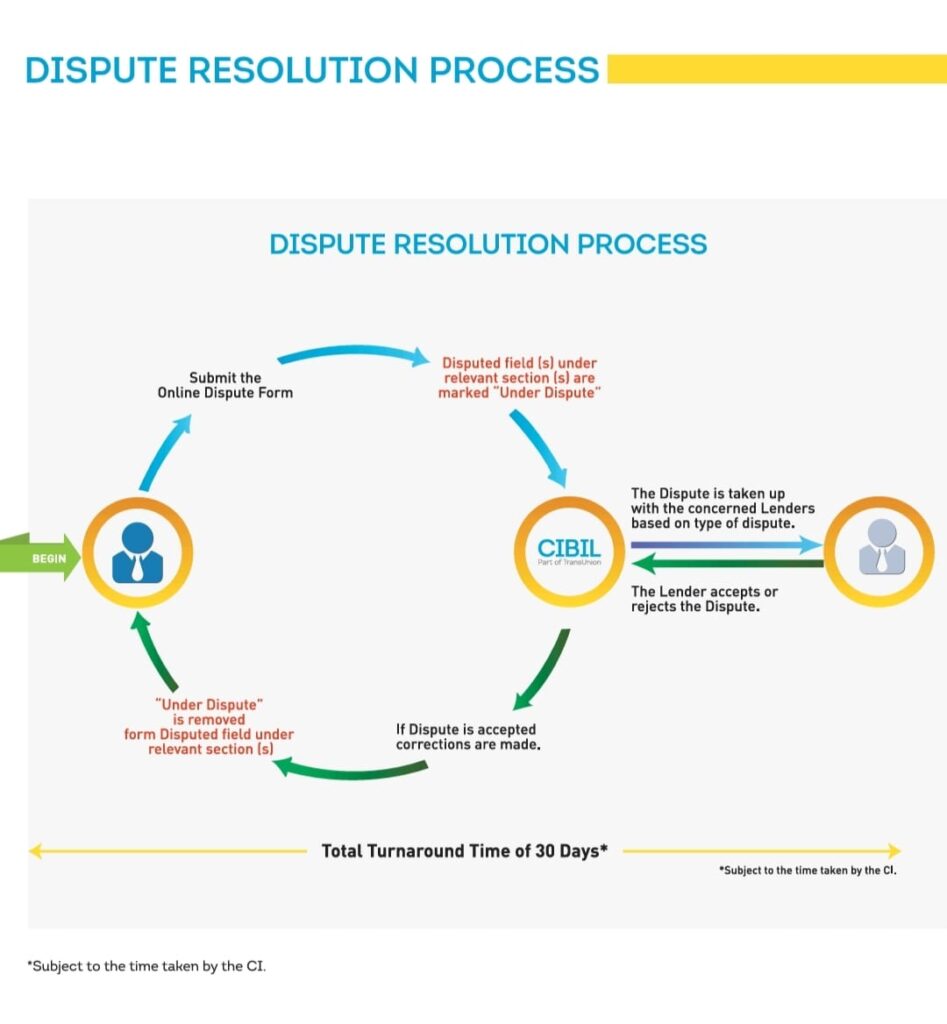

A bad or poor CIBIL score does not put an end to your financial journey but it will slow you down. There is no need to fret if you have a bad CIBIL score, you can always change it before it’s too late. It is important to check your CIBIL report for errors if you notice that you have a bad report. If your CIBIL report is not updated or if it has errors you need to get it corrected immediately. The individual can address the concern with CIBIL’s “dispute resolution” if there is an error in the report. But if the bad score is due to poor financial decisions, it is important to improve your CIBIL score by making payments on time and not defaulting. Because at the end of the day CIBIL score does play a very crucial role in determining how easy your financial journey is.

How to improve CIBIL Score

A good credit score is essential for obtaining loans, credit cards, and other financial products on favorable terms. Here are some effective strategies to improve your credit score:

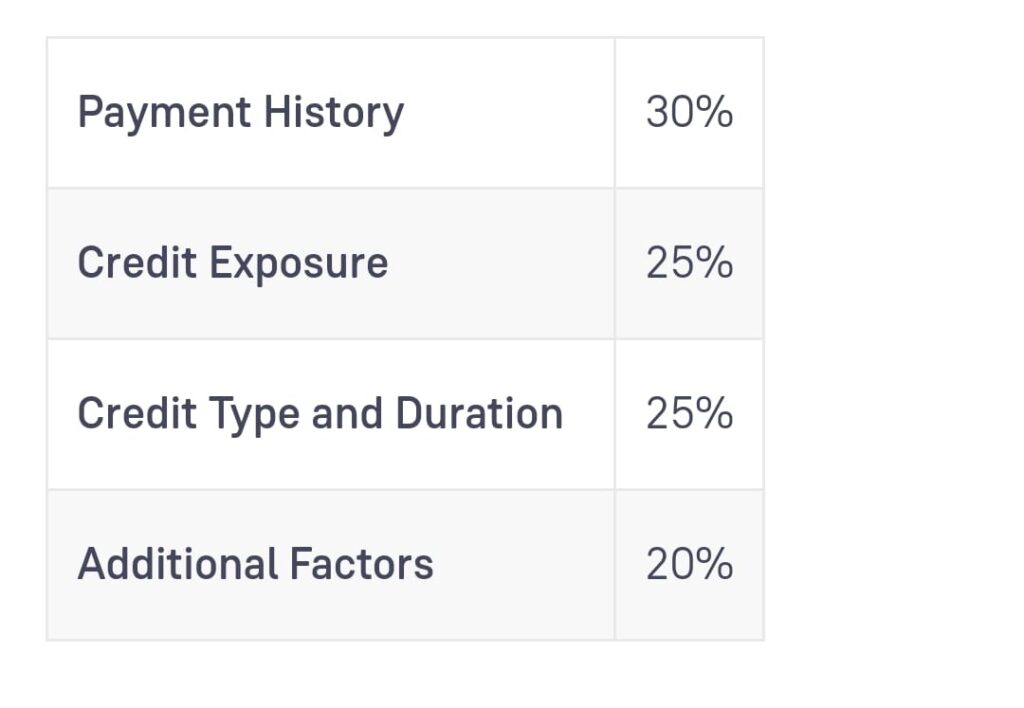

Factors that make up your CIBIL Score: Source- Groww

1. Pay Bills on Time:

- Consistency is key: Make sure to pay all your bills, including credit cards, loans, and utilities, on or before the due date. Late payments can negatively impact your credit score. This has a high effect on your credit score.

- Make sure you don’t miss any loan or credit card payments by more than 29 days—payments that are more than 30 days late might be reported to credit bureaus and damage your credit ratings.

2. Reduce Credit Card Debt:

- Limit spending: Try to keep your credit card balances low compared to your credit limits. High credit utilization ratios can lower your credit score.

- Create a repayment plan: Develop a strategy to pay off your credit card debt as quickly as possible. Consider consolidating debt into a lower-interest loan if necessary.

3. Check Your Credit Report Regularly:

- Identify errors: Review your credit report from all three major credit bureaus (Equifax, Experian, and TransUnion) at least once a year. Look for any errors or inaccuracies that could be affecting your score.

- Dispute errors: If you find any errors, dispute them with the credit bureaus and the relevant creditors.

4. Limit New Credit Inquiries:

- Avoid excessive applications: Too many credit inquiries in a short period can lower your credit score. Only apply for new credit when absolutely necessary.Your credit score can be impacted temporarily if you make too many accounts or requests in a short amount of time.

5. Maintain a Mix of Credit:

- Diversify your credit: Having a mix of different types of credit, such as credit cards, loans, and mortgages, can positively impact your credit score. Credit max has a low impact on your credit score.

6. Be Patient:

- Credit scores take time: Improving your credit score takes time and consistent effort. Don’t get discouraged if you don’t see immediate results.

Additional Tips:

- Consider credit counseling: If you’re struggling with debt or credit management, consider seeking professional credit counseling.

- Avoid closing old accounts: Keeping older credit accounts open, even if you’re not using them, can help your credit score.

- Credit Utilisation :It is recommended not to exceed 30% of your credit limit.

- Credit Age: It measures how long you have held credit accounts by calculating the average age of all your accounts. It has a medium affect on your credit score .

- Setting up automated payments for the minimal amount required will assist you to avoid skipping a payment (provided you don’t overdraft your bank account). If you’re having difficulties paying a payment, contact your credit card company immediately away to explore hardship alternatives.

- It is important to check your CIBIL score before applying. Note that multiple rejections from banks can also negatively affect your credit report.

By following these strategies, you can significantly improve your credit score over time and gain access to better financial opportunities.Sources and related content

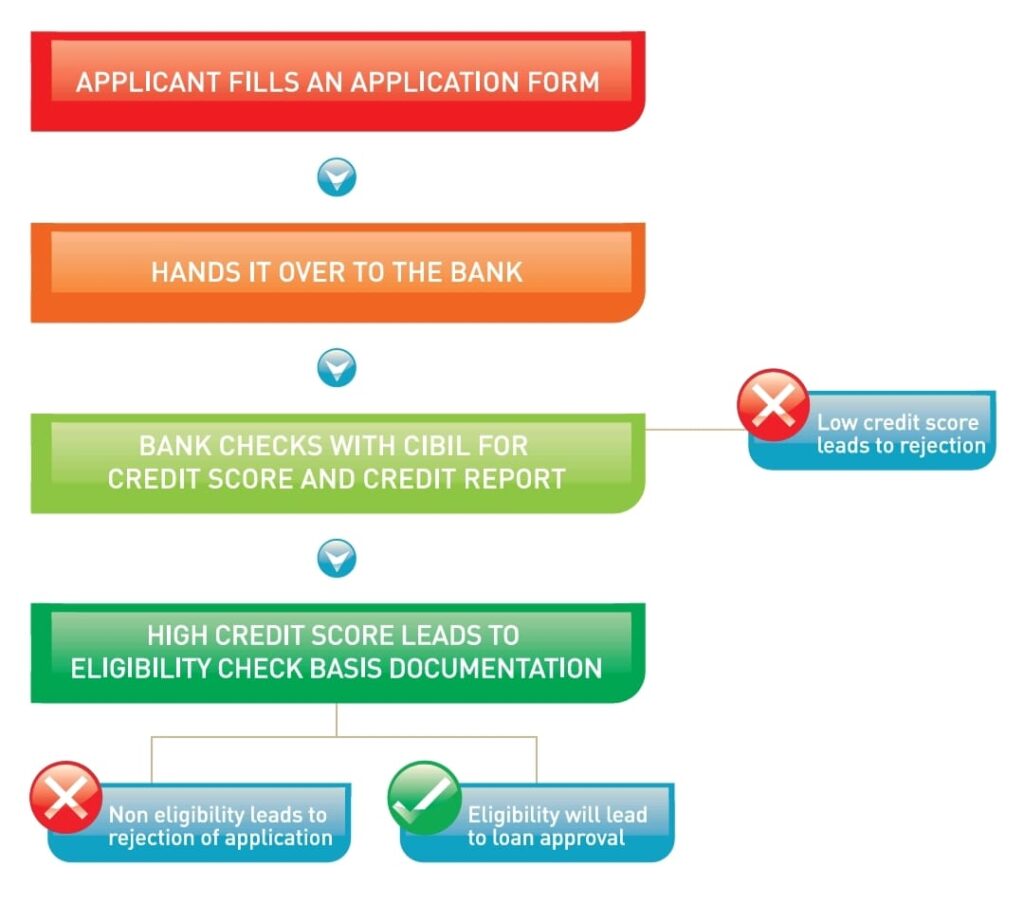

Loan Approval Process

Loan eligibility is determined using information such as income, current EMIs, and credit score. Once credit score meets the lenders internal credit policy criteria they then analyse the documents to understand some key points before applying for loan process.

Source :CIBIL

What are the types of disputes /Errors that can be raised with CIBIL ?

- Personal Information : Information such as name ,date of birth, PAN Card and address

- Account information

- Ownership: Make sure all personal details and account belongs to you.If an account does not match raise a dispute.

- Duplicate Account :If the same account is reflected more than once ,you can get this rectified.

CIBIL Score is a helpful metric that financial institutions may use to assess a person’s or a business’s capacity to repay their loan. Those who keep their credit score high will benefit from attractive benefits. I would request to keep a healthy score if you want to avail credit cards or loans.